"we are at an inflection point where the assumptions that shaped the global markets for the last three decades are no longer true" - Speaker [00:00:00]

Disclaimer: Orignal content owned by or sourced from third parties. It does not represent the views of 'Nuggets' platform or it's team. AI is used extensively across this platform including for summaries. Accuracy is not guaranteed, there can be mistakes. Any info or content on this platform is not a financial, legal, or investment advice. Do your own research. Refer for complete disclosures:- Terms of Use · Full Disclaimer

The global economy is undergoing a profound structural regime shift from a system optimized for globalization and efficiency to one driven by national security, resilience, and multipolar geopolitical competition.

Accelerated by unsustainable levels of sovereign debt (particularly in the US), nations are weaponizing supply chains, adopting industrial policies, and engaging in an AI and semiconductor "arms race."

For investors, this means the old playbook of chasing asset-light, globally integrated companies is dead; the new era requires reallocating capital toward real assets, defense, energy security, and the physical infrastructure powering artificial intelligence.

3. Chronological Table of Contents

[00:00:00] - Introduction: The End of Unipolar Globalization

Security Over Efficiency: Supply chains are being fundamentally redesigned. Corporations and nations are shifting from "Just-in-Time" (lowest cost) to "Just-in-Case" (redundancy and security).

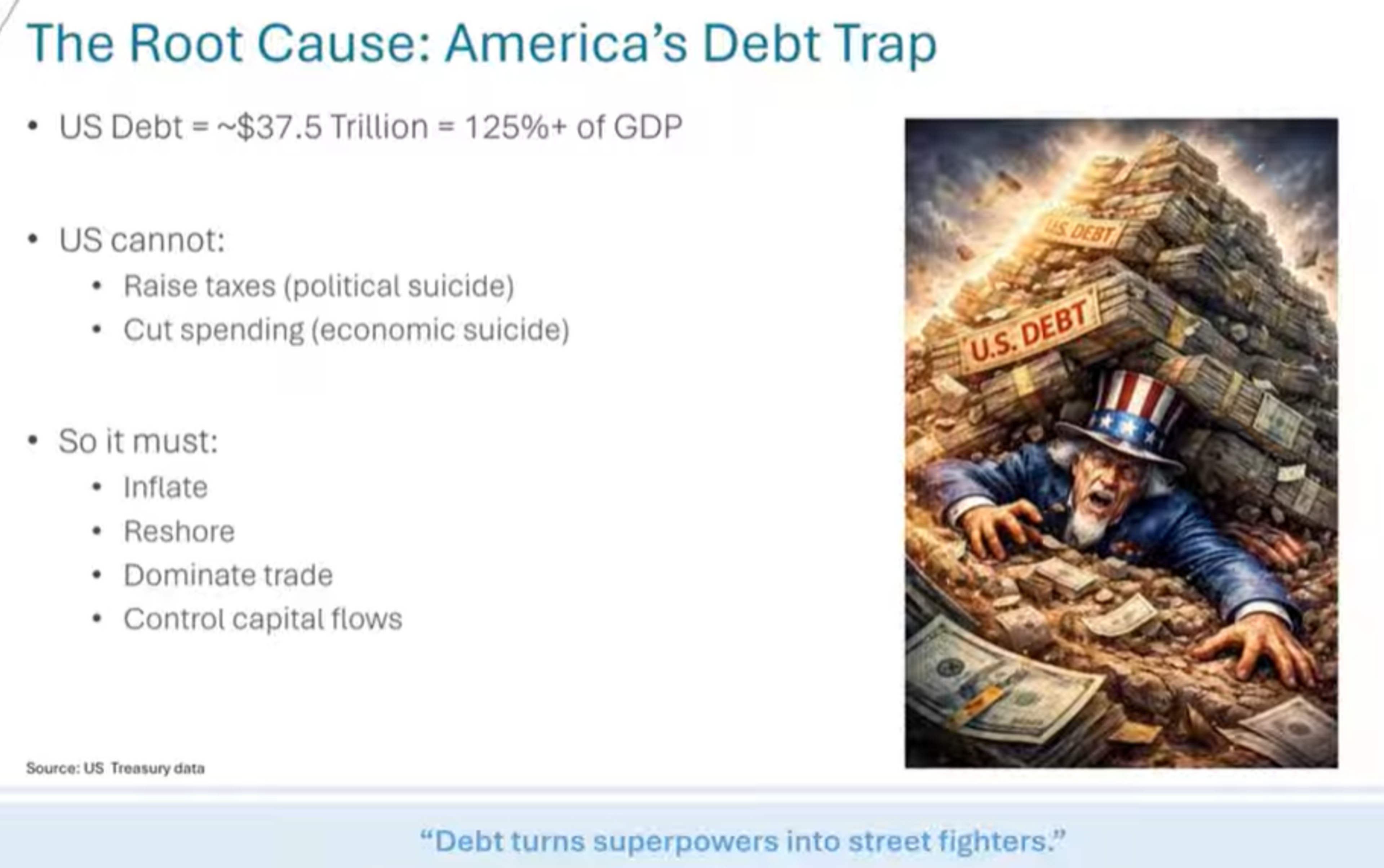

Debt Drives Policy: US sovereign debt limits traditional economic policy choices. The inability to raise taxes or cut spending makes inflationary policies and tariffs mathematically inevitable to manage the debt burden.

The Return of Real Assets: Capital is rotating out of financialized, asset-light business models and moving back into capital-intensive, asset-heavy sectors like manufacturing, grids, and infrastructure.

AI is Geopolitical Leverage: Artificial intelligence and semiconductors are no longer just consumer tech; they are the modern equivalents of nuclear deterrence and oil. Controlling these choke points is a matter of national survival.

Resources are the New Currency: Foreign policy is now supply chain policy. Diplomacy is driven by access to critical minerals, energy, and fabrication capacity rather than ideology.

Defense is Non-Discretionary: Security spending is rising globally regardless of GDP growth. Governments are optimizing for deterrence, leading to multi-year order books for defense and cybersecurity firms.

The presentation begins by establishing that the globalization assumptions of the last 30 years—characterized by flat-earth optimization, lowered costs, and extended supply chains—are dead. The 2021 semiconductor shortage served as the wake-up call, proving that efficiency without resilience is fragile.

Historically, empires (Roman, Byzantine, Ottoman, British) follow a predictable pattern: they rise via productivity, peak through financialization, accumulate massive debt, and eventually cede power as the center of gravity shifts. We are currently witnessing the messy rebalancing of the global system from a unipolar US-led order to a multipolar world.

The US is currently burdened with staggering national debt, severely limiting traditional policy choices. Historically, almost every country reaching these debt-to-GDP levels has defaulted or debased its currency.

Because raising taxes is politically suicidal and cutting spending risks severe recession, the only viable path is inflating the debt away while simultaneously reshoring production to protect domestic jobs. This mathematical constraint—not necessarily ideology—is what drives aggressive, muscular trade policies and tariffs.

The speaker argues that Donald Trump is a symptom of a system that was already breaking under the weight of high sovereign debt, fragile supply chains, and rising inequality. While his style is abrasive and transactional, the actual trajectory of his policies (tariffs, reshoring, tech controls, energy security) is structurally inevitable.

This is evidenced by the fact that the Biden administration continued these industrial policies (e.g., the CHIPS Act), and nations like Japan, Korea, and European countries are equally focused on self-reliance.

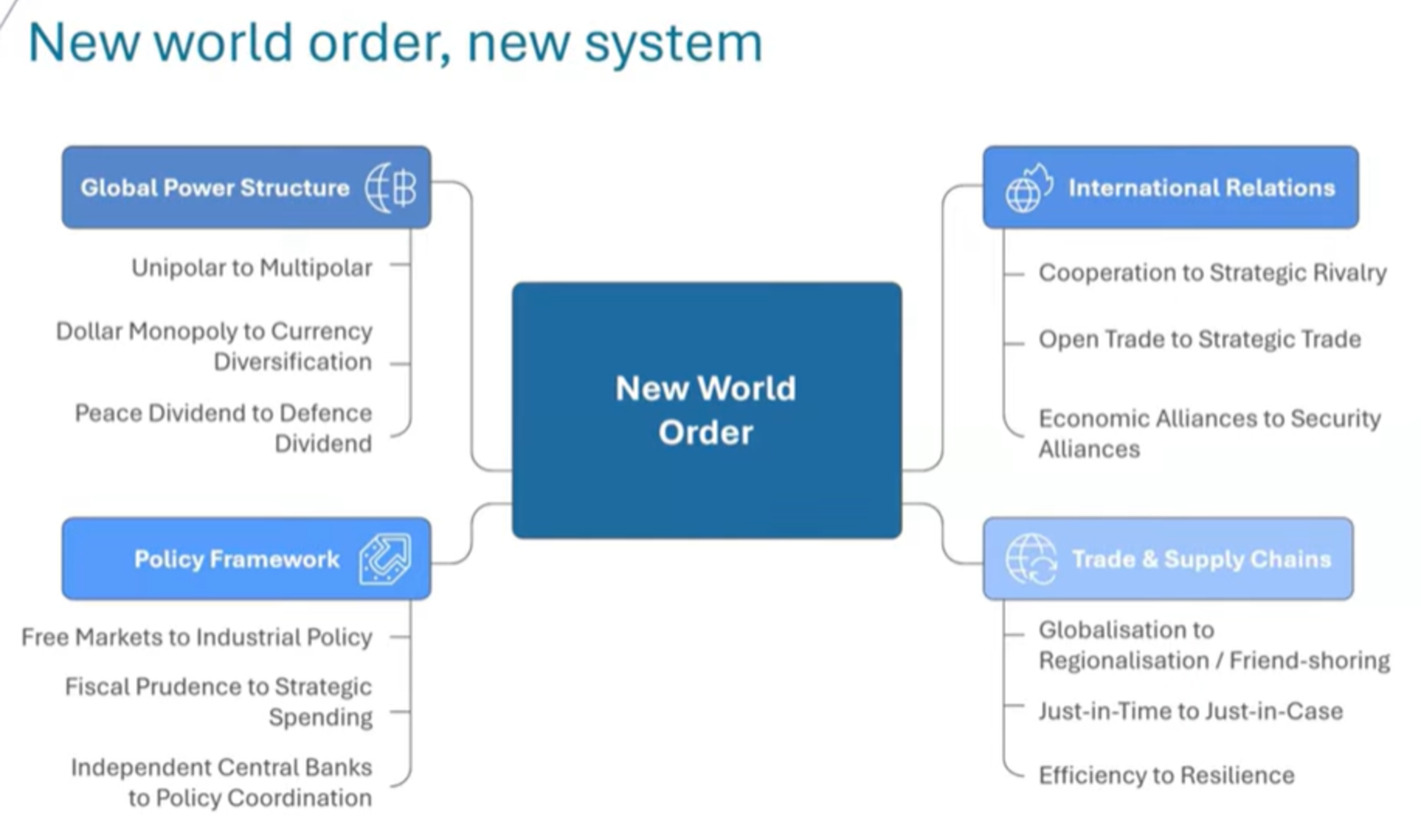

Post-WWII institutions (UN, IMF, WTO) and trade pacts (NAFTA) were designed to maximize global economic integration. However, that architecture is being dismantled in favor of bilateral agreements and secure supply chains. National security has officially merged with economic policy.

As a result, capital allocation is shifting. Investors who thrived on asset-light, margin-expansion models over the last decade will struggle. The new era favors capital-intensive, asset-heavy businesses that build physical resilience: factories, power generation, and logistics.

New World OrderNew World Order ConsequencesThe Economic Consequences

To explain the current geopolitical dynamic, the speaker introduces the "TRUMP" framework:

Treasury distress (debt limits choices),

Reshoring (rebuilding domestic capacity via tariffs),

US supremacy waning (prompting aggressive reassertion of power),

Multipolarity (co-operation replaced by strategic control), and

Power politics (leverage and sanctions replace diplomacy).

In this multipolar world, power is distributed: China is the factory, the Middle East is the energy banker, Russia is the military disruptor, and India is the democratic scale player. Capital flows will become highly selective based on these shifting alliances.

Debt Dictate's Trumps Playbook

The TRUMP FrameworkMultipolarity Changes EverythingNow You UnderstandThe End Game

Modern manufacturing and global dominance now rely on "Chips + AI + Automation". Taiwan is identified as the single most critical geopolitical choke point. AI is described as the "new nuclear arms race" and the ultimate productivity lever required to grow out of massive public debt.

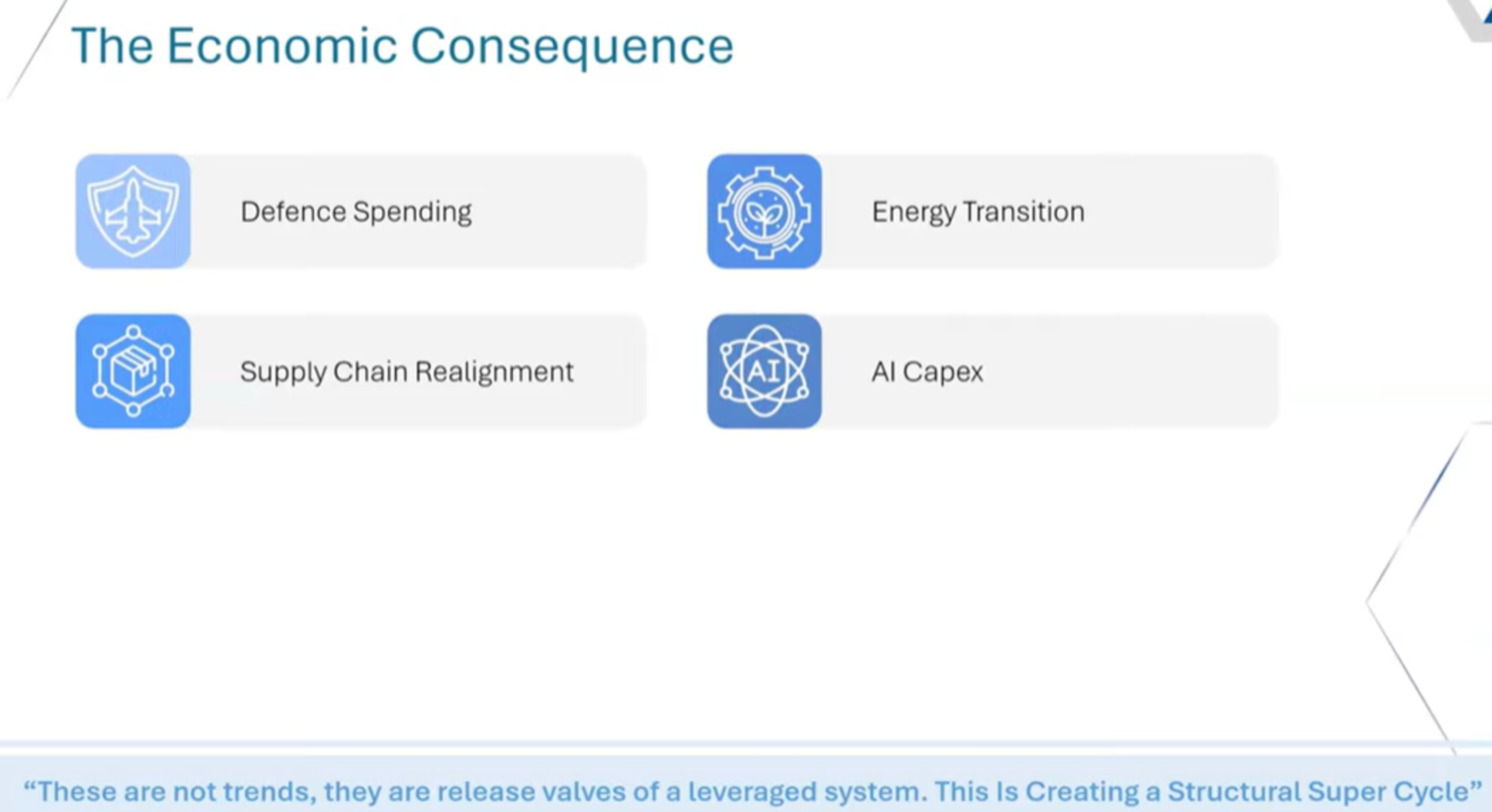

Consequently, the investment landscape has permanent new winners: defense (deterrence), energy security (redundancy over cost), industrial reshoring, and the physical infrastructure required to power the digital world (semiconductors, data centers, power grids, nuclear energy, and cybersecurity).

AITrump LensBusiness World ImpactPicks & Shovels

6. Data & Figures

Data Point

Value

Context

Timestamp

Historical Timeline

5,000 years

The span of human history showing the rise and predictable fade of global empires.

The 2021 Semiconductor Shortage: The speaker uses the 2021 auto-chip shortage to illustrate how global efficiency without resilience is fragile. It proved that chips were not just economic components, but geopolitical leverage, halting assumptions about the safety of globalization. [00:01:03](https://www.youtube.com/watch?v=YSEcXpMHTlY&t=0h1m3s)

The Fall of Historical Empires: The speaker points to the Romans, Byzantines, and Ottomans. Each empire felt permanent, relying on roads, geography, or trade routes. Yet, they all faded through the same pattern: rising productivity, followed by financialization, massive debt, ballooning administrative/military costs, and eventual transition to new centers of power. [00:02:46](https://www.youtube.com/watch?v=YSEcXpMHTlY&t=0h2m46s)

The Hollowing Out of Middle America: As an example of globalization's hidden costs, the speaker notes how NAFTA and free trade delivered lower costs and high corporate profits, but hollowed out the manufacturing communities of Middle America—first losing out to Japan, and subsequently to China. [00:13:12](https://www.youtube.com/watch?v=YSEcXpMHTlY&t=0h13m12s)

8. Core Frameworks & Mental Models

The Five Stages of Empire Transition:

Application: Used to pinpoint exactly where the US is in its historical lifecycle.

Just-in-Time vs. Just-in-Case (Efficiency vs. Resilience):

Application: A mental model for capital reallocation. For 30 years, companies optimized for "Just-in-Time" lowest-cost global sourcing. Today, they must optimize for "Just-in-Case" survival, requiring redundant, domestic, asset-heavy investments in physical infrastructure. [00:00:53](https://www.youtube.com/watch?v=YSEcXpMHTlY&t=0h0m53s)

Geopolitics on the Balance Sheet:

Application: A framework for valuing companies. Governments and corporations are no longer evaluating investments (like defense spending or building domestic solar supply chains) based on pure Return on Investment (ROI). They are optimizing for deterrence and national security, making these sectors structurally highly valued regardless of normal economic cycles. [00:31:05](https://www.youtube.com/watch?v=YSEcXpMHTlY&t=0h31m5s)

The T.R.U.M.P Framework:

Application: Used to decode aggressive US foreign policy not as madness, but as mathematical necessity. Treasury constraints, Reshoring mandates, US supremacy waning, Multipolarity rising, and Power politics replacing diplomacy. [00:21:48](https://www.youtube.com/watch?v=YSEcXpMHTlY&t=0h21m48s)

People:Donald Trump & Joe Biden - Mentioned as executing the exact same structural industrial policies despite differing outward styles. Samir - A colleague referenced who covers the emerging markets impact of these shifts. Ankita - The host/moderator of the presentation.

Institutions:UN, IMF, World Bank, NATO - Highlighted as legacy post-WWII institutions that are struggling to enforce outcomes in a newly multipolar world.

10. Speakers & Credentials

Speaker: Unnamed ValueQuest representative (likely a Senior Portfolio Manager or Macro Strategist) delivering a macro thesis on global markets.

Ankita: Host/Moderator for ValueQuest.

ValueQuest: The financial/investment institution hosting the presentation.

11. Actionable Next Steps

Audit Portfolio for Fragility: Review current investments and reduce exposure to asset-light companies heavily dependent on single-source, cross-border supply chains (especially those reliant on China).

Rotate into "Picks and Shovels" of AI: Look beyond software companies and invest in the physical constraints of artificial intelligence: semiconductors, data centers, cooling technology, and power grid upgrades.

Overweight Defense and Cybersecurity: Treat the defense and cybersecurity sectors as non-discretionary utility allocations, as global governments will continue multi-year spending cycles regardless of macro-economic slowdowns.

Target Energy Independence: Seek opportunities in domestic energy production, nuclear, and critical minerals (copper, lithium), as nations pay a premium to secure supply chains away from geopolitical rivals.

Jul 13, 2026

Yanis Varoufakis | Closing Keynote | Thursday 18th June 2026 | Web3 Foundation

"Politics is who does what to whom... who has the power to do to make you do stuff." Yanis Varoufakis 00:02:36 https://youtu.be/WZeuKyUs9hM?t=2m36s "We have created machines and machinery—network machines—that are not produced means of pro…

Sovereign Defaults

51 out of 52

The historical track record of countries defaulting after hitting 130% debt-to-GDP.