Geopolitical shocks do not tend to affect UST yields independent of their impact on oil prices | Deutsche Bank

{kind=link}

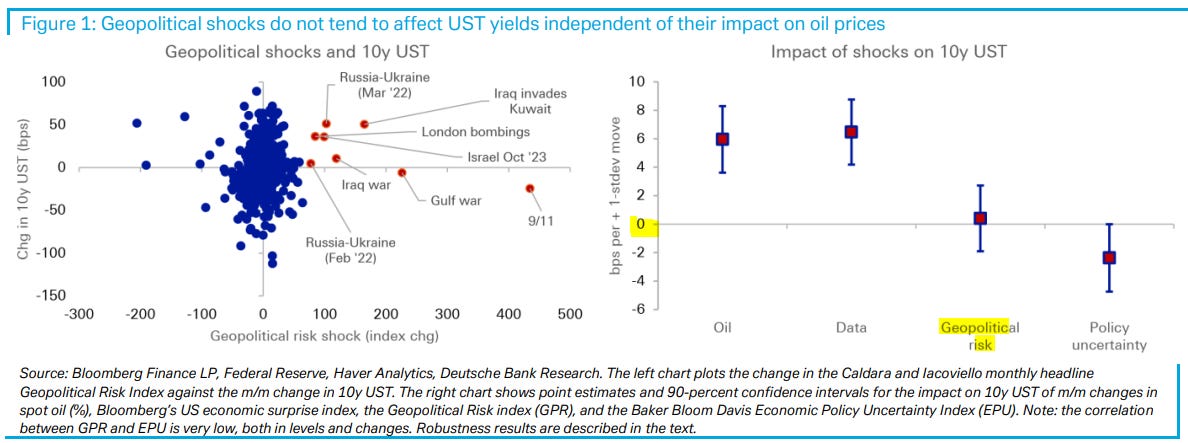

The results indicate that positive oil price moves and data surprises significantly lift yields, higher policy uncertainty lowers them, and geopolitical shocks have no direct impact.

These findings are robust to running the analysis on daily instead of monthly data, entering the geopolitical and policy uncertainty indexes in levels rather than changes, and including the lagged change in the 10y UST as a regressor to control for any yield-momentum effects. Together, this suggests that, as far as UST yields are concerned, the main mechanism / variable to track on current Iran developments is the price of oil.

References

Disclaimer: Orignal content owned by or sourced from third parties. It does not represent the views of 'Nuggets' platform or it's team. AI is used extensively across this platform including for summaries. Accuracy is not guaranteed, there can be mistakes. Any info or content on this platform is not a financial, legal, or investment advice. Do your own research. Refer for complete disclosures:- Terms of Use · Full Disclaimer

More nuggets

Jul 15, 2026

What Americans Need to Understand About China Ft. Kevin Rudd | 14 Jul 2026 | The Ezra Klein Show

"He saw that the trend of Chinese history was China was a great power when it was a unified and able to keep foreign adversaries under control and divided; and China collapsed as a great power when neither of those propositions held true."…

Jul 15, 2026

The Strong Do What They Can and Suffer What They Must | Jonathan Kirshner | 13 Jul 2026

"The strong do what they will and the weak suffer what they must... both of those are radically decontextualized. Graham Allison made a book about the so called Thucydides trap that drew on that first sentence... both of those are based on…

Jul 14, 2026

How America Overtook Britain as the World's Economic Superpower | 8 Jul 2026

"The transfer of economic supremacy from Britain to the United States wasn't a single dramatic event... It was a slow grinding multigenerational process full of financial maneuvering, industrial brute force, two catastrophic world wars, an…